Mississippi ERC Tax Fraud Sentencing: Patricia Jones Ordered to Pay $1.4M

Document Desk voice

Ready when you are.

Status, July 1 source check: source-cleared for a taxpayer-accountability, financial-fraud, courts, and pandemic-relief fraud ledger. The controlling case source is the U.S. Attorney’s Office for the Northern District of Mississippi release dated June 30, 2026.

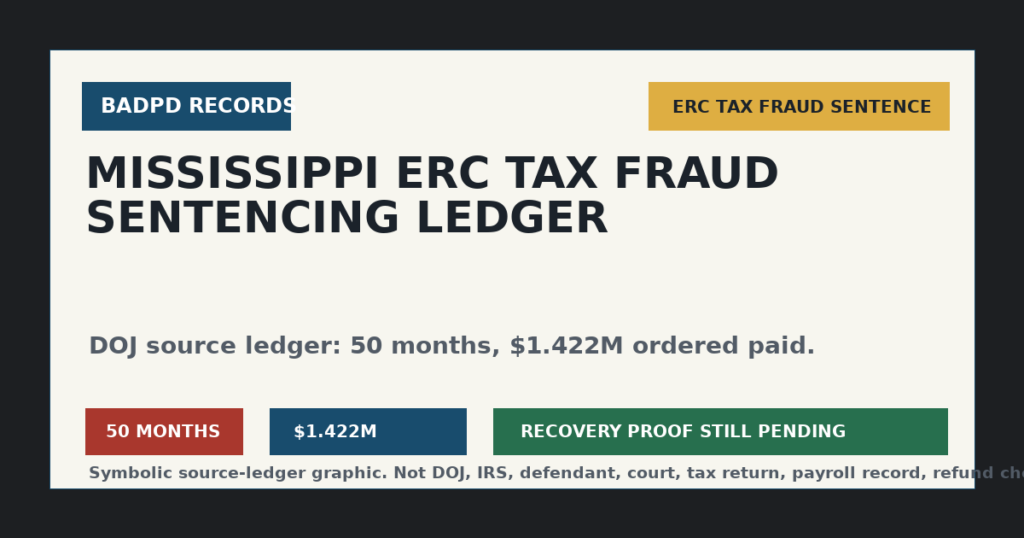

DOJ says Patricia Jones, 44, of Lamar, Benton County, Mississippi, was sentenced by Senior U.S. District Judge Sharion Aycock after previously pleading guilty. The sentence is 50 months in prison, 3 years of supervised release, and an order to pay $1,422,022 to victims.

According to DOJ, Jones submitted false and fraudulent IRS forms to obtain Employee Retention Credit funds. DOJ says the ERC was designed to encourage employers to continue paying employees during the effects of the COVID-19 pandemic. The release says Jones submitted forms on behalf of herself and others, attempted to claim more than $3.8 million in fraudulent refunds, and generated more than $1.4 million in fraudulent IRS payments to Jones and others.

That makes this a taxpayer-money case, not just another sentencing notice. The public record should separate three numbers: the attempted refund amount, the fraudulent-payment amount DOJ says was generated, and the court-ordered payment amount. DOJ puts those numbers at more than $3.8 million attempted, more than $1.4 million generated, and $1,422,022 ordered paid. BadPD is not treating those as interchangeable.

What DOJ Confirms

- Patricia Jones, 44, of Lamar, Benton County, Mississippi, was sentenced in federal court.

- DOJ says Jones had previously pleaded guilty.

- Senior U.S. District Judge Sharion Aycock sentenced Jones to 50 months in prison.

- The sentence includes 3 years of supervised release.

- The court ordered Jones to pay $1,422,022 to victims.

- DOJ says Jones submitted false and fraudulent IRS forms to obtain ERC funds.

- DOJ says Jones submitted forms on behalf of herself and others.

- DOJ says the attempted fraudulent refund claims exceeded $3.8 million.

- DOJ says the scheme generated more than $1.4 million in fraudulent payments by the IRS to Jones and others.

- IRS Criminal Investigation investigated the case.

- Assistant U.S. Attorney Clay Dabbs prosecuted the case.

What Is Still Missing

- The final judgment and full restitution schedule.

- Whether the $1,422,022 ordered payment has been collected, partially collected, or remains unpaid.

- Whether forfeiture was ordered separately from restitution.

- Whether public docket records identify business entities, accounts, preparers, promoters, or other participants.

- Whether any appeal, post-judgment motion, or related case update is filed.

- Whether the IRS stopped, paid, recovered, or credited back every claim linked to the scheme.

Not Established

- That all $3.8 million in attempted refunds was paid out.

- That the government has recovered all money described in the release.

- That every person included in DOJ’s phrase “Jones and others” has been publicly identified.

- That all ERC claimants are suspect.

- That every ERC error is criminal fraud.

- That this article gives tax, legal, or eligibility advice.

Why The ERC Context Matters

The IRS Employee Retention Credit page describes the ERC as a refundable tax credit for certain eligible businesses and tax-exempt organizations that had employees and were affected during the COVID-19 pandemic. IRS says the requirements differ depending on the period claimed and that the credit is not available to individuals. That context matters because the Jones release is specifically about claims tied to ERC funds.

IRS says it remains concerned about improper ERC claims and urges taxpayers to review claims and resolve incorrect ones. The agency says employers that submitted ineligible claims may be able to avoid future problems by withdrawing an ERC claim if the credit has not been paid, or if a check was received but not cashed or deposited. That is context for readers, not a separate fact about Jones.

IRS also says eligible employers generally must have paid qualified wages and must meet a qualifying COVID-era condition, such as a government-order suspension, a required decline in gross receipts during the relevant period, or recovery startup business rules for certain 2021 quarters. Those eligibility ideas matter here because payroll, employees, wages, operating status, and tax-return facts are the records that separate a lawful ERC claim from a false one.

BadPD is not going to turn an ERC enforcement case into a blanket smear on small businesses. A legitimate employer with records is not the same thing as a fraudulent filing. The public-interest problem is that fraudulent refund requests can make honest taxpayers wait longer, add enforcement costs, and make an already complex credit harder to navigate.

The Public-Money Question

The strongest follow-up is the money trail. A prison sentence tells the public that the criminal case reached a punishment stage. It does not automatically prove taxpayers have been made whole. The judgment should be checked for restitution, payment schedule, interest, forfeiture, financial conditions of supervised release, and any collection language. If the court order identifies the victim or victims more clearly than the press release, that should be added in a later update.

DOJ says Jones attempted to claim more than $3.8 million in fraudulent refunds. It also says more than $1.4 million in fraudulent IRS payments were generated. The difference between attempted claims and paid claims is important. An attempted false claim can be criminal even if not every dollar is paid. But the public-accountability question after sentencing is narrower: what got out, what was recovered, and what remains owed.

The release says payments were generated to Jones and others. That phrase should stay narrow until public records support more. It does not name every other person. It does not identify whether all “others” were charged, uncharged, witnesses, businesses, accounts, or recipients. A hard records piece should not guess identities or roles. It should preserve the gap and check the docket.

Fraud Enforcement Without Campaign Copy

The DOJ release frames the case as part of a broader federal fraud-enforcement effort. BadPD can note that as an official statement, but the article should not become government public relations. The public does not need slogans. It needs dates, names, amounts, sentence terms, source limits, and a recovery watch.

The same discipline applies to IRS guidance. The IRS pages are official context for ERC eligibility and scam warnings, but they do not add Jones case facts beyond the DOJ release. They do help readers understand why improper ERC claims remain a live enforcement and taxpayer-service issue. They also help keep the article useful for people who may need official correction or reporting routes.

IRS warns employers to be wary of ERC advertisements that tell them to apply for money when they may not qualify, and warns that incorrectly claimed credits may have to be repaid with penalties and interest. IRS lists warning signs such as large upfront fees, fees based on a percentage of the refund, eligibility promises made before reviewing tax facts, and pressure based on the false idea that every business qualifies.

Those warnings are relevant because the ERC market attracted aggressive marketing and confusion. They are not proof that any specific preparer or promoter was involved in the Jones case. If later court records identify a preparer, promoter, business entity, bank account, or return-preparation channel, BadPD should update with the record. Until then, the official fact is that Jones was sentenced for false and fraudulent IRS forms in an ERC-related scheme.

Public-Service Route

For readers worried about their own ERC claim, the responsible path is official confirmation. Use IRS pages, reputable tax professionals, and official correction or appeal procedures. Do not rely on social-media posts, refund pitches, or generic promises that a business qualifies without reviewing its facts. BadPD is not giving tax advice. Eligibility is official-confirmation-needed.

The IRS tax scams page points taxpayers toward official fraud and scam-reporting channels. That matters because tax enforcement should not only punish after the fact; it should also help people avoid bad filings before money leaves the Treasury. A public-accountability article should point to official sources while keeping the criminal case facts confined to the defendant and the court record.

Why The Local Details Matter

This case is not only a national ERC story. DOJ identifies Jones as a resident of Lamar in Benton County, Mississippi, and the release came from the Northern District of Mississippi. Local identification matters because federal fraud cases often read abstractly from a distance. A county-level frame makes the accountability question concrete: public money was allegedly pursued and paid through federal forms, but the enforcement burden, court coverage, and restitution follow-up still land in a real district with real taxpayers.

The local frame should still be handled carefully. The DOJ release identifies Jones and the federal case. It does not accuse the town, the county, local officials, local businesses, or any local tax office of wrongdoing. BadPD should keep the article aimed at the federal case record and the public-money recovery question, not at community guilt by geography. The location helps readers search and follow the docket; it does not broaden the accusation.

Mississippi readers also have a practical reason to care about the exact amount ordered. Federal sentences can create a headline number, but restitution and collection can remain unresolved for years. If $1,422,022 is ordered paid, the public should be able to check later whether payments are made, whether garnishment or other collection tools are used, and whether the obligation survives after prison. That is a records question, not a vibes question.

Records To Pull Next

The next useful record is the final judgment. It should confirm the prison term, supervised release term, restitution amount, special assessment, forfeiture if any, and payment schedule. If the judgment includes a list of victims or a sealed restitution schedule, that distinction matters. A public article can report the existence of sealed or limited records without guessing what is inside them.

The plea agreement and factual basis, if publicly available, would also help separate admitted facts from sentencing-stage claims. DOJ says Jones pleaded guilty earlier, but the press release does not reproduce the entire plea record. The plea documents may identify the charge, statutory basis, offense conduct, loss calculation, relevant conduct, and any agreement about cooperation or restitution. Those are the records that should control any future expansion.

The sentencing memorandum, if public, may explain how prosecutors and the defense framed the loss amount, payment ability, role in the offense, and guideline range. Those documents can be more detailed than a press release, but they are still advocacy documents unless adopted by the court. BadPD should label them accordingly. The judgment and court orders carry more weight than a party’s sentencing argument.

IRS-CI materials may eventually add enforcement context, but they should not be used to inflate the case beyond the court record. A press release can say the investigation was done by IRS Criminal Investigation. It does not by itself prove collection status, asset tracing, or recovery. If later IRS-CI or DOJ records say money was recovered, BadPD should quote the amount and date, then compare it against the ordered payment and the fraudulent-payment figure.

How To Read The Three Dollar Figures

The $3.8 million figure is the attempted-refund figure in DOJ’s description. It tells readers the scale of the claims submitted or attempted. The more-than-$1.4 million figure describes fraudulent payments DOJ says were generated by the IRS to Jones and others. The $1,422,022 figure is the amount the court ordered Jones to pay to victims. Those figures are close enough to be confusing, but they do different work.

A careful follow-up should not say “$3.8 million stolen” unless a court record establishes that the full attempted amount was paid or legally treated as loss. It should not say “$1.4 million recovered” unless collection records prove recovery. It should not say “$1,422,022 restitution” if the judgment labels the amount differently. For now, the careful sentence is this: DOJ says more than $3.8 million was attempted, more than $1.4 million in fraudulent IRS payments was generated, and the court ordered Jones to pay $1,422,022 to victims.

That wording may be less dramatic, but it is more useful. It lets readers track the money from attempted claims to payments to court-ordered repayment. It also prevents a common fraud-story error: treating charge numbers, loss numbers, restitution numbers, forfeiture numbers, and recovered-money numbers as if they all mean the same thing. They do not.

What A Responsible Update Would Add

A later update should add only records that change the public picture. A docket entry showing the judgment is useful. A collection update is useful. A related defendant, business entity, promoter, preparer, or bank-account record is useful if it is tied to court documents. A generic reminder that ERC fraud exists is not enough for a new post unless it is linked to official enforcement, new recovery, or a service resource readers can use.

If the case produces appeal records, BadPD should preserve both statuses: sentenced in district court and appeal pending. If the court later amends restitution, the new amount should replace or supplement the old amount with dates. If the government later announces recovery, the article should say whether recovery is cash, property, forfeiture, offset, restitution payment, or some other category. Public money deserves exact labels.

Follow-Up Calendar

This article should be checked again when the judgment, restitution schedule, collection status, or any related docket entries become public. The useful follow-up is not another headline saying “tax fraud is bad.” The useful follow-up is a receipt check: sentence entered, restitution ordered, money collected or still owed, appeal status, and any additional public records naming entities or participants.

- Next court-record check: final judgment, restitution schedule, forfeiture if any, and supervised-release financial conditions.

- Money-lane check: compare the $3.8 million attempted-refund figure, the more-than-$1.4 million fraudulent-payment figure, and the $1,422,022 ordered-payment figure.

- IRS/DOJ watch: look for later ERC enforcement, recovery, correction, scam-warning, or promoter-case updates.

- Source discipline: keep IRS pages as program context unless a later official record ties specific guidance or actors to the Jones case.

Source Ledger

- DOJ NDMS Patricia Jones sentencing release, June 30, 2026

- IRS Employee Retention Credit page

- IRS ERC eligibility checklist

- IRS tax scams page

Source status note: DOJ NDMS controls the Jones sentencing facts. IRS pages are official context for ERC eligibility, improper-claim warnings, correction paths, and tax-scam reporting. No third-party reporting or social posts are used as standalone facts.

Featured image is symbolic editorial artwork created for BadPD. It is not DOJ, IRS, Patricia Jones, Lamar, Benton County, a court, a tax return, a payroll record, a refund check, or evidence photography.

Send receipts for the desk to research

Send corrections, missing records, police-accountability tips, good-cop public-service receipts, government/court/war leads, recall alerts, or property-tax help resources. Tips are leads only until BadPD verifies records.

Links, dates, agency names, docket numbers, bodycam IDs, recall numbers, forms, and official pages.

Every tip is a lead, not a fact. The desk checks records before publishing.

Use advertising inquiry when you want clearly labeled sponsor space or available ad placements on BadPD.